- Ecom CFO Notebook

- Posts

- Ecom CFO Notebook - eComFuel's 2026 trends report and 5 stars literacy

Ecom CFO Notebook - eComFuel's 2026 trends report and 5 stars literacy

Sam Hill

April 10, 2026

Ecom CFO Notebook is a (mostly) strategic finance publication for $10M+ ecommerce operators.

What I write comes from the patterns, problems, and decisions from our client work at Ecom CFO - providing brands outsourced CFO, accounting, and financial operations.

I write because I enjoy it. And because it brings in great clients.

My inbox is open - respond to this email or schedule a call if you want to be one of them.

This week we’re back to hardcore finance.

But I did want to thank you all so much for the kind responses from last week’s edition. Kiara and I had such an incredible weekend with family and friends.

While I was out, I hope you saw eComFuel Trends Report.

Andrew Youderian (founder of eCom Fuel) teased it a few weeks back.

When I finally saw it this week, I printed out all 60+ pages, went on a walk, and recorded a 40-minute voice note with you on my mind.

The report is based on 300 operators with $3.5 billion in combined revenue. There’s a lot of really cool, different types of data. As someone who publishes a quarterly benchmark report, I can appreciate how big of a lift this is.

The report is 60+ pages. There’s a lot to go through, and I have a lot of thoughts.

But I combed through it with my finance lens specifically. My job as a CFO — and where I think I can actually help you the most — is curating and pointing your attention to the areas that are most relevant to the 8-figure DTC brand.

And staying true to what I know the most, which is finance.

There’s a lot of data in this report about sales channels, competitive advantage, business model shifts — all of which is interesting. But the one section that really stood out to me is the section on Financial Intelligence (page 19).

Andrew has been talking about this a lot on LinkedIn and his podcast. I’m biased, but I share his opinion that financial literacy is extremely correlated with better financial business outcomes.

The survey asked founders to rate their own financial literacy on a scale of one to five, and it shows that higher financial literacy correlates with better financial outcomes.

Surprise, surprise.

But the report doesn’t define what three stars versus four stars versus five stars actually looks like.

I wanted to share my own definition — with practical, actionable steps — from my experience working with hundreds of brands.

What is DTC financial literacy?

I don’t care what knowledge you hold in your head.

What matters are the behaviors, actions, and systems you’ve set up.

Finance degrees don’t necessarily correlate with better business outcomes - and thank god because very few of you have one.

Moreover, taking an accounting course, or prompting Claude to teach you about accounting, is not going to do much for you if your books are bad, if you can’t read your financials, or if you’re not actively engaging with your CFO.

What separates 3 stars from 5 stars isn’t credentials or coursework.

What separates 3 stars from 5 stars are habits, activities, and systems.

If you’re reading this newsletter, you’re probably already operating at a three minimum.

You’ve got some financial infrastructure in place. Someone is doing your books. You’re showing up to meetings. The basics are covered.

But we’ve already established that easy mode is over. We need to add more stars.

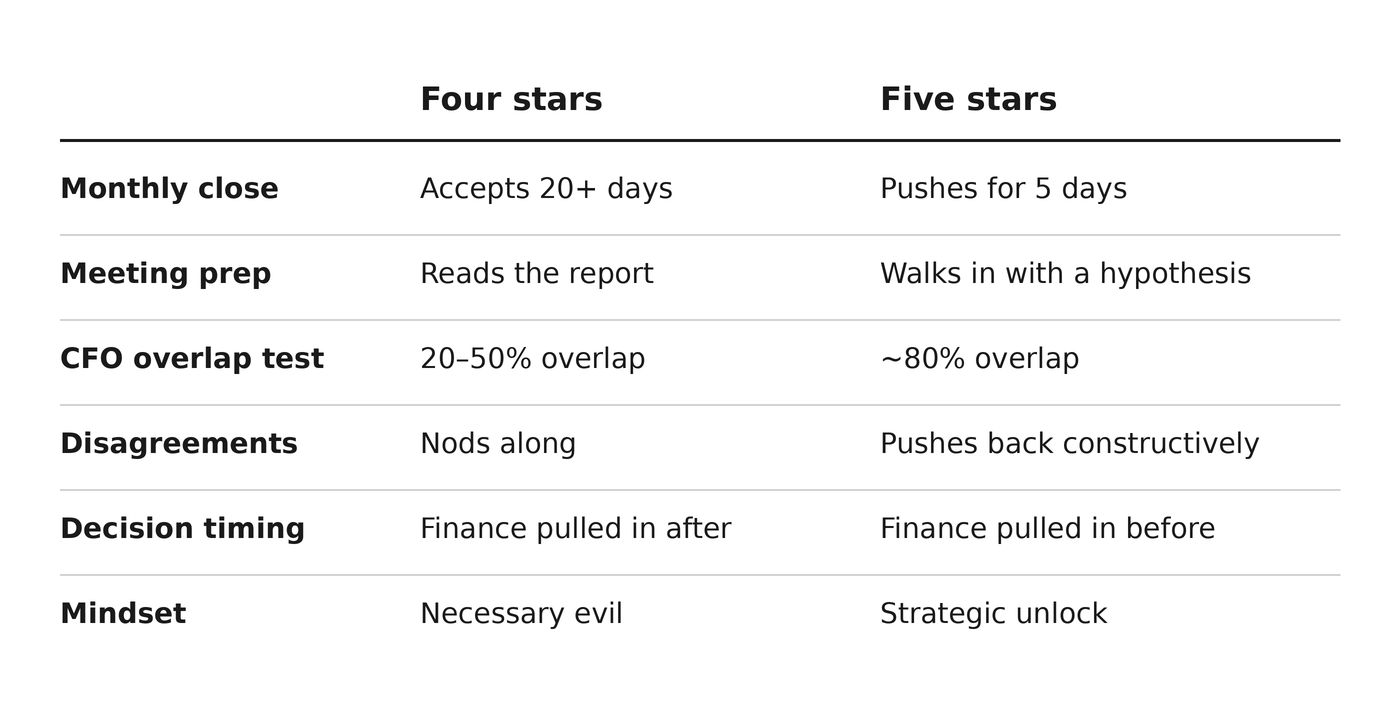

Four stars: you're fluent but…

At four stars:

You understand everything being presented to you

You’re talking to your CFO as a peer

You’re showing up to finance meetings prepared — you’ve actually opened the report before the call, you’ve glanced at the variance from last month, you have a couple of questions queued up.

You’re asking follow-up questions in real time.

When the CFO says “gross margin compressed 3 points,” you don’t just nod — you ask why.

You can make connections across the P&L on your own: you see ad spend up and conversion rate down in the same month, and you connect those two dots without anyone having to point it out for you.

But your read of the financials is still mostly surface level. You look at the report and you can call out the obvious things — “we had a sale last month, margins were down” — but the deeper question of how much that sale actually contributed to or detracted from contribution margin isn’t one you could answer or determine how to answer easily.

You know something needs further digging when you see it. That’s the four-star instinct.

But you’re not always clear on exactly where to go or what questions to ask next. You’ll tell your CFO “we should look into that” and then wait for them to come back with the analysis.

A five-star founder would already have a hypothesis about where the issue is and what data would confirm or disprove it.

The other tell: at four stars, you’re mostly reacting to what your CFO puts in front of you. You’re a great audience. You’re engaged.

But finance is still something that happens to you on a monthly cadence — it’s not yet something you’re actively driving.

Five stars: the most financially fluent founders I know

At five stars, you’ve delegated key parts of finance, but you still really know what’s going on. This is an important distinction.

Five stars doesn’t mean you’re doing all of finance yourself — in fact, the opposite. The five-star founder has a CFO, a controller, a bookkeeper, probably an FP&A person.

They’ve built the team. But they’ve also built enough fluency that they could hold their own if they had to.

Here’s the most tangible way I can describe it.

If you and your CFO were both given your financials and 30 minutes to review it independently, then compared notes, your findings would overlap about 80%.

Same callouts, same areas of concern, same questions about what to dig into next. You wouldn’t catch everything they catch — they’re the specialist for a reason — but the big stuff, the things that actually matter for the next decision, you’d both flag.

Compare that to four stars, where the overlap might be 20% to 50%. Or three stars, where the founder is mostly reading the report for the first time in the meeting itself.

At five stars, you’re also having constructive disagreements with your CFO — not just nodding along. You’re pushing back when something doesn’t look right, because you already have a view on what the numbers should be saying.

You’ve done the mental math. You know roughly what gross margin should be this month given the promo cadence, and if it comes in 2% off, you’re asking why before they have a chance to walk you through it.

If a lender asks about your accounting policy, you could answer the question directly or have a document ready. You’re not waiting for someone to interpret the data for you. The meeting becomes a conversation about what to do — or walking through the financial implications of a potential decision — not a summary of what happened.

There are two other dimensions I see that consistently separate the fours from the fives.

Speed

Five-star clients are demanding. Things happen faster around them, and that’s not an accident — it’s a byproduct of fluency. When you actually understand what’s in the financials, you stop accepting mediocrity in how they’re produced and delivered.

A four-star founder accepts a 20-day close because that’s what they’ve always had. A five-star founder asks why it’s not 5 days, and pushes until it is.

They want the financials closer to real time because they’re actually using the financials to make decisions — and a 20-day-old number isn’t useful when you’re deciding what to do next week.

I think about the client I referenced a few newsletters ago. He was doing his own vendor research, having very pointed strategic calls about our scope, and constantly pushing for faster closes, faster reporting, faster turnaround on questions. That kind of pace is exhausting if you’re not fluent — because you’re asking for things you can’t fully evaluate.

But when you’re fluent, the speed compounds. You ask better questions, you get answers faster, you make decisions faster, and the whole finance function starts operating at the cadence of the business instead of lagging behind it.

Mindset

Five-star founders see finance as a core part of their activity — not a necessary evil they dread. They’ve become fluent enough that it’s not painful anymore.

The monthly close isn’t something they put off; it’s something they look forward to because it confirms what’s happening in the business.

They view finance as an unlock that opens the door for a lot of other things. Better hiring decisions. Better inventory decisions. Better marketing decisions. Better partnership terms. Better lender conversations.

None of those get unlocked without a financial foundation, and the five-star founder feels that connection viscerally — they’re not just intellectually convinced finance matters, they’ve experienced what it feels like to make a bad decision because they didn’t have the financial picture, and they’ve built the habit of not letting that happen again.

This is the real shift. Going from “finance is a thing I have to deal with” to “finance is integral to why we’re in business — we exist to generate a profit, and finance should be in mind for every decision.”

It’s an important seat at the table for any strategic decision making — not just something you have to do at month-end.

Final Thoughts

Most founders I talk to assume they’re at a three or a four. The ones who are actually at four or five know it, because their finance meetings feel different — less time spent on what happened, more time spent on what to do about it.

If I had to point to one habit that separates the fours from the fives, it’s this: filtering decisions through finance before you take action, not after.

Marketing brings you a new channel test. Operations wants a second warehouse. A supplier offers a deal that cuts COGS by 12%. All of those are potentially good things.

The financial lens is asking what each one does to cash, what the working capital impact is, and what happens if it doesn’t work.

The tariff data in the report is a good illustration. Forty percent of brands didn’t raise prices at all in response to tariffs. I’m assuming most of the ones who did raise prices arrived at that number through gut instinct, or by asking peers what they were doing.

The five-star move is to run the actual math before you act. My guess is that raising those prices would have paid for not only the tariffs, but probably the cost of a CFO as well.

The next time you’re about to make a decision, consider finance’s seat at the decision table.

— Sam

Looking for more? Some of our most popular posts:

2026 Annual Benchmark Report: Key insights from financials across 30+ companies – including revenue growth, margins, ad spend, and more.

2026 Revenue Planning Guide: Our report on macroeconomic indicators, Shopify GMV trends, and same-store revenue benchmarks to give operators a clear, data-backed outlook for 2026.

The issue with KPIs: Everyone has tons of data, but doesn’t know what to do with it. This is my take on managing the right metrics.

Responsibility Map: I walk through how to define who owns, participates in, and supervises every key finance & accounting deliverable

Did someone forward this to you? If you like it, you can subscribe here