- Ecom CFO Notebook

- Posts

- Ecom CFO Newsletter - Introducing Our Q1 P&L Benchmark Report

Ecom CFO Newsletter - Introducing Our Q1 P&L Benchmark Report

Sam Hill

June 06, 2025

Be Informed. Take Action. Keep Your Ass Solvent

Welcome to the Ecom CFO Notebook - weekly finance clarity for ecommerce founders building more profitable businesses.

Why is it called Notebook? And what’s with the generic squared background?

I still manage my most important tasks and write my most interesting thoughts by hand in a notebook lined with little squares. I buy them by the dozen.

Felt like a fitting name for the newsletter.

Sam here, and this week, we’re releasing our full Q1 P&L Benchmark Report.

We analyzed data from nearly 20 companies, with revenues ranging under-$10M to $50M+, and pulled out trends in revenue, gross margin, contribution margin, EBITDA and more.

We also share benchmarks on everything from ad spend to ROAS, overall G&A, marketing as a percent of revenue, and more.

Our continued goal is to publish the best benchmark data in our industry - giving you the data to understand your own performance.

Someone forward this to you? If you like it, you can sign up here.

And if you want help talking through it, get a spot on my calendar below.

In this week’s edition

📈 Featured Topic: Our Q1 P&L Benchmark Report

💼 DTC DealFlow + Talent Flow: Buy, Sell, Hire, Connect

🔗 Best Links + Resources: Keeping Secrets Makes You Un-Copyable… Scaling Acquisition Value… How To Stay Lean While Growing

FEATURED TOPIC

(what got the most thinking time)

Key Insights from Our Q1 P&L Benchmark Report

Every month, when we sit down with clients, we hear some version of the same question:

“What are you seeing in the market”?

We see the books across dozens of $1M to $100M+ brands, and have a very unique view into how the market’s changing.

We want to share that.

Here are a few of the big findings…

1. The Best Brands Are Still Growing, Despite The Environment

Among companies we tracked, half saw revenue increase in Q1.

But gains weren’t experienced evenly.

Companies with less than $50M in net revenue generally suffered, with a 5-6% decline at the 50th percentile. Yet even the worst of $50M+ companies saw significant growth (it’s good to be big).

There is hope though.

Brands of every size saw growth at the 95th percentile.

The macro headwinds are there but some companies are winning

2. Wholesale continues to expand

Half of our sample companies do some kind of wholesale business, and across every cohort, revenue in that category is up.

For brands under $50M, wholesale is the fastest-growing revenue category.

This likely would have been true for all cohorts.

But one of the $50M+ companies is crushing so hard on meta ads that, even though wholesale grew significantly, it still represents a smaller percent of overall revenue than Q1 last year.

Overall, revenue in this segment grew ~9-40% across our cohorts, and representing a bigger chunk of the overall revenue pie than it did 2024

3. Gross margin was about even

We didn’t observe significant changes in gross margin.

The slight decline in companies under $50M happens to correlate with growth in their Wholesale revenue. So, not necessarily cause for alarm.

But worth calling out is that there are very few companies in the 8- to 9-figure range that don’t have at least 70% margins.

I would argue it’s a defining characteristic of brands that get to that size.

Also, the spread between best- and worst-performers in our under $10M cohort is much broader, with more than 30 percentage points between 5th and 95th percentiles.

4. Contribution Margin Was Up

We were surprised to see contribution margin was up for many companies, despite revenue down.

As we’ve said again and again (and as the data below supports), you should be targeting a baseline CM of at least 30% - with some exceptions for dropshippers and high volume/commodity resellers.

Brands under $10M saw a decline in contribution margin, which makes sense when you see that the two key drivers – gross margin and ROAS – were also down.

Among $10-$50M brands, CM is up, even though gross margin was flat and ROAS was down. That could be due to things like:

Change in channel mix

Pick / pack / ship efficiency - cheaper to ship wholesale orders in bulk than individual DTC orders (though this would be relatively minimal)

Investing in non-variable marketing, and it’s paying off

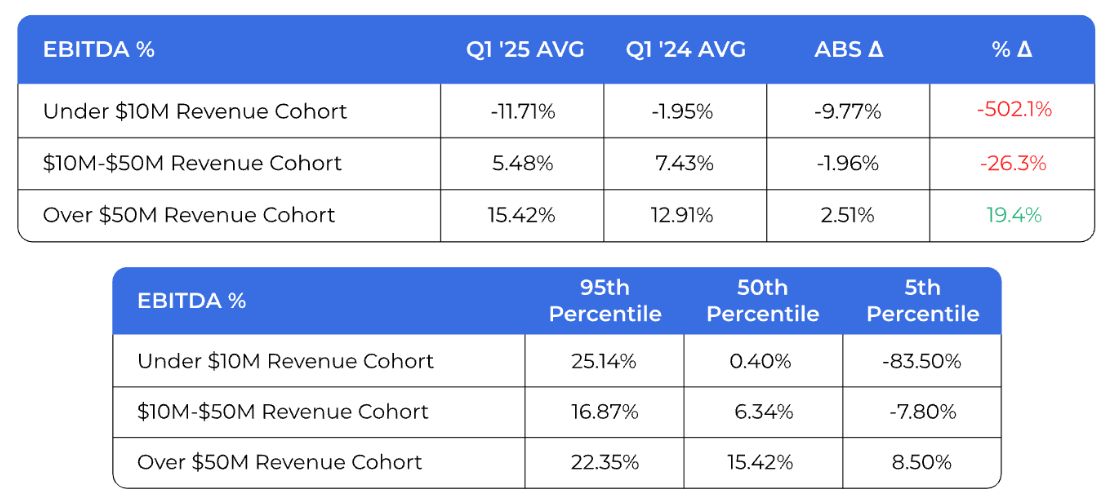

5. EBITDA was a mixed bag

Only half of our sample companies saw EBITDA percentage grow in Q1.

Not surprising. First quarter is typically the worst, with tons of post-holiday returns, an inventory squeeze, etc.

But the averages hide an important truth – some grew EBITDA a lot, despite headwinds.

Two brands from our sample were up more than 200% YoY.

One, a 7-figure brand, went from -$70k in EBITDA to +$70k (finally becoming profitable), and the other, an 8-figure brand, went from ~$130k in EBITDA to $400k+.

This reinforces a main takeaway from this report – great companies are finding ways to grow.

For Even More…

Check out the full report for all this, plus more data, insights, and CFO perspective on things like…

Price, volume, mix trends for Q1

Gross margin discipline and how it’s paying off

Client anecdotes (like the brand that cut ad spend to $0 while growing revenue)

And more…

And if you have an audience of ecom founders, and you’d like us to come do a detailed breakdown for them (e.g., blog post, podcast interview, newsletter write-up, etc.) hit reply and let me know.

🛠️ Work With Us

Ecom CFO is one of the only fractional finance and accounting firms that specializes exclusively in 7- to 9-figure DTC clients. This email is part of our effort to share industry-best insights with founders, for free.

But when you're ready, here’s how to get in touch:

📊 Compare Your P&L to Other Private Brands

We analyzed financials across 30+ companies to show you exactly what happened – including revenue growth, margins, ad spend, and more. The full report is free and un-gated. Use it to battle test your 2025 plans.

💼 DTC Dealflow + Talent Flow

As trusted advisors, specializing in 7- to 9-figure ecom brands, we get an early look at a lot of the most important financial and hiring decisions clients and colleagues make, and are always happy to help with introductions…

Seeking Acquisition: Sleep accessory brand, with $1m+ in rev L365. Reportedly has great margins, solid inventory, is profitable, and has domestic/offshore manufacturing lined up

Seeking Acquisition: A $2m skincare brand (mostly wholesale/retail) selling for inventory+

Seeking Acquisition: A few of our larger clients are in the early stages of exploring acquisition. If you’re a buyer writing checks for more than $10M, message me privately.

Seeking Role: COO/GM with end-to-end ecommerce experience optimizing the value chain to drive growth. Experienced leading business operations, new market development, marketing, technology, logistics, and building teams. Runs the EOS management system. A great fit for a design/product focused CEO who needs a business operator. Open to fractional roles.

Seeking Talent: Dr. Paul Saladino’s company, Lineage Provisions is looking for their next Director of Growth. Fully Remote.

Seeking Talent: Boston-based Force Factor is bringing on a staff accountant.

If you’re buying, selling, or hiring in this space, and want more visibility, reply to this email or grab a call with me here. Everything you say is fully confidential.

🔗 Best Links & Resources

My team reviews industry insights every week to stay current. We curate the best, so you don't have to...

1. Keep Secrets: This article, by Brian Lange, over at FutureCommerce, was fascinating. It’s dense, and worth the read – exploring how brands can create things that stay relevant in an age where it’s harder and harder to do anything truly novel. The last 300 words or so are worth reading twice.

2. Scaling LTV & Acquisition Value: Been enjoying Fan Bi’s conversation with Dave Rekuc of Bamboo Earth, which has this fascinating membership model (different from subscriptions) that helped drive 30X growth post-acquistion

3. Scalability School: This new podcast hosted by Andrew Foxwell, Zach Stuck, and Brad Ploch is very actionable. Episode one hits the ground running, with Meta creative they wish they’d tested sooner, and this week’s ep, on how to stay lean, aligns well with many of the most important findings from our quarterly report.

🧭 Footnotes

Other Resources Clients Find Helpful: Here are a few tools we've built for clients and find ourselves sharing over and over...

If you missed last week, we talked about how to actually USE benchmark data in your company, and you can find it here.

Until next time,

-Sam